Managed Conflict, Fractured Energy Architecture: Hormuz Disruption Structural, Resolution Uncertain — Natural Gas and Uranium Long, Oil and Iron Short

CORE MACRO THEME

The US-Iran war entered its 95th day inside a managed-chaos phase: the Trump-Netanyahu confrontation, Israel’s expanding Lebanon ground offensive, and Iran’s suspension threat on negotiations progressed simultaneously. Bloomberg’s primary source Stulberg (Georgia Tech) projected oil prices could remain elevated through Q1 2027 even if a deal were signed today; Rystad calculated that in a re-escalation scenario prices could reach 180 dollars per barrel by August. The transmission mechanism is dual: first, the physical constraint keeping approximately 27 percent of global seaborne oil trade through a restricted Hormuz; second, Qatar LNG infrastructure requiring up to five years of repairs.

SECTOR IMPACT MAP

Natural Gas and LNG Corridor — EXPANDING / MEDIUM-LONG

Natural gas sits 6.78 percent above its 30-day average at 3.21 dollars. This deviation traces directly to the Hormuz constraint pushing Qatar LNG export into operational uncertainty: OilPrice.com analysis puts Qatar LNG facility repair timelines at up to five years. Simultaneously, Australia’s Ichthys LNG project faces active strike threat from the Offshore Alliance unions. Panama Canal Strategic Updates confirms that European buyers, including Germany’s Uniper, are exploring Canadian Pacific LNG as a long-term Hormuz alternative. Both pressures push in the same direction — physical supply constraint deepens, spot premium holds. Medium-term demand anchor remains solid.

Uranium and Nuclear Infrastructure — EXPANDING / MEDIUM-LONG

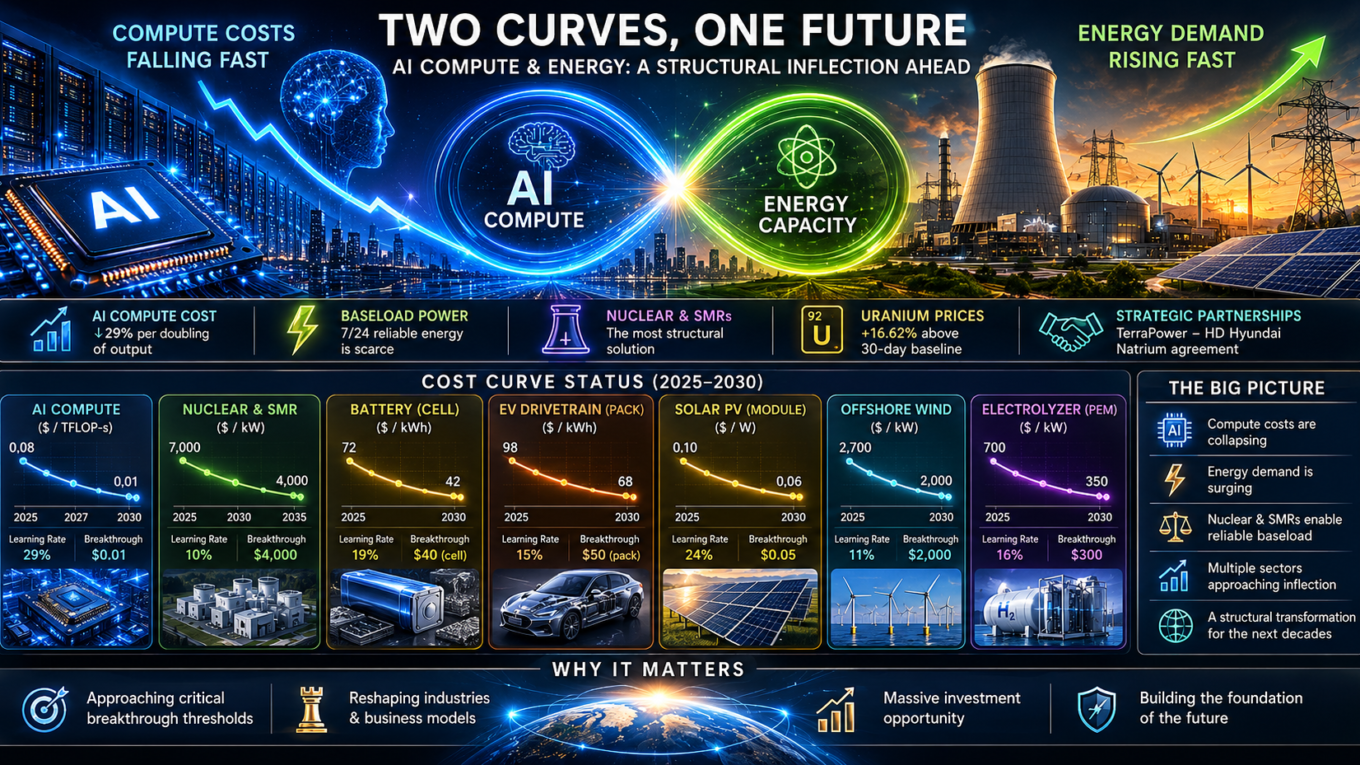

Uranium sits 6.19 percent above its 30-day average at 84.25 dollars. This is not incidental; it reflects nuclear repricing as baseload energy security solution in a world where fossil reliability collapsed. Power Magazine Nuclear data is concrete: Sweden saw Blykalla and Studsvik file separate applications for up to 1.7 GW at two sites, with the government committing 3.7 billion dollars to the Ringhals SMR project; Ontario directed a 300 million dollar pre-development agreement for Bruce C; TerraPower broke ground on the Natrium reactor in Wyoming. World Nuclear News confirmed Kazakhstan and Russia signed a state-to-state nuclear plant financing agreement. Multiple independent structural nodes are moving in the same direction. LONG horizon SMR cost deflation compresses the primary thesis — see Counter-Thesis below.

Oil — DECLINING / SHORT-MEDIUM

Oil sits 8.11 percent below its 30-day average at 93.86 dollars. Strategic Memory node R-1 already diagnosed the core anomaly: Hormuz attack saturation with flat VIX and DXY together signal de-escalation pricing, not blockade pricing. Today’s data adds a new dimension: the Trump-Netanyahu confrontation and Iran’s negotiation suspension threat returned as live variables threatening the de-escalation scenario. The price is caught between the two; structural direction is down, but short-term risk is symmetric. Rystad’s 180-dollar scenario is conditioned on a real Hormuz closure; current data prices managed crisis not that scenario. OilPrice.com expert commentary warns Iranian control of Hormuz could be permanent regardless of political outcome. KISA: avoid. MEDIUM: downside pressure persists.

Iron — DECLINING / MEDIUM

Iron sits 8.45 percent below its 30-day average at 91.22 dollars. The causal chain: Hormuz constraints raise industrial input costs, which suppress manufacturing output, which compresses steel demand. Hellenic Shipping News reports Capesize market partial recovery driven by Pacific activity; this floors incremental downside but does not reverse the direction. Medium-term underweight maintained.

BTC — RISK APPETITE BAROMETER — READING NEGATIVE

BTC sits 10.40 percent below its 30-day average at 69,432 dollars. Mandatory outlier analysis applies: the gap is large, direction negative, yet VIX sits 2.56 percent below average. The apparent contradiction has two structural readings. First: BTC has decoupled from traditional risk-off signaling — AI equity rally and war confusion redirected liquidity into equities, not crypto. Second: mining economics suffering from energy cost increases may have created structural earnings pressure. Under either reading, BTC does not provide risk-on confirmation this cycle. Avoidance sufficient.

Gold — CRISIS BAROMETER — NON-TRIVIAL ABSENCE OF PREMIUM

Gold sits 0.84 percent below its 30-day average at 4,556 dollars. The absence of a safe-haven premium confirms the market prices managed ceasefire, not active escalation. Bloomberg reported that India’s Reserve Bank may have sold a portion of its gold reserves to defend foreign currency assets, adding incremental supply pressure. The flatness in gold is itself a data point confirming the de-escalation narrative has not been abandoned, even as diplomatic signals contradicted each other.

DXY — DOLLAR DOMINANCE BAROMETER — NEUTRAL

DXY at 99.08, only 0.18 percent above average. No global liquidity stress signal, and no dollar strengthening. Bloomberg confirmed the yuan strengthened to its highest level against a trade-weighted basket since 2022, reflecting regional safe-haven flows into Chinese assets. DXY provides no independent directional signal; consistent with the managed-conflict thesis.

US10Y — RATE ENVIRONMENT — AMBIGUOUS HEADWIND

US10Y at 4.47, 0.27 percent below average. Mild decline signals partial safety bid. However, Bloomberg confirmed new Fed Chair Kevin Warsh is approaching an employment-data threshold that could trigger a rate hike; additionally the 30-year Treasury topped 5 percent for 11 consecutive days in May. This rate environment compresses long-duration equity valuations. Active headwind for LONG-horizon growth positions.

Copper and Aluminum — EXPANDING / MEDIUM

Copper sits 2.82 percent above average at 6.64 dollars. Bloomberg sourced Andrew Grove, chairman of Copper Intelligences, confirming data center buildout is pushing demand ahead of supply growth. Copper carries dual structural support: war-driven supply constraint and AI infrastructure demand acceleration operating simultaneously.

Wheat and Food Security — WEAK SIGNAL / MEDIUM

Wheat sits 0.81 percent below average, appearing calm. However Bloomberg reported Australia’s 2026/27 winter wheat crop is forecast to fall more than 26 percent due to dry weather and war-related input cost increases. Japan faces banana shortages linked to the Middle East conflict. These signals confirm food inflation diffusion from the war zone into broader supply chains. Current wheat flatness may be obscuring structural year-end risk; monitor, do not position yet.

Technology Counter-Thesis (LONG Horizon)

With ARK Invest Research and Power Magazine Nuclear signals both active, the counter-thesis node is mandatory. NUCLEAR_SMR sits 0.09 percent below average, GRID_INFRA 0.02 percent lower — these are short-term fluctuations, not trend. The structural force is cost deflation: as SMR reactors approach commercial scale, with Hermes 2 and Natrium construction now underway, the levelized cost comparison against LNG and oil-based power will structurally compress the long-term competitiveness of fossil fuel energy. This force does not price within 6 months; it operates on a 3-to-5 year cycle. The current NATG long thesis remains valid within that window; exit timing should track SMR production cost benchmarks as they are published.

INSTRUMENT CASCADE

Natural Gas Sector. BUY / LONG. [SISTEM] NATG — Hormuz constraint placing Qatar LNG in minimum 5-year operational uncertainty, plus Australian Ichthys strike risk, sustain spot premium support. NATG 6.78 percent above 30-day average. Data: Yahoo Finance NG=F. Invalidation condition: verified and full normalization of Hormuz transits, or Qatar return to full LNG export capacity. Time horizon: MEDIUM. Secondary: [SISTEM] LNG_EQ — enter after primary confirmation, same invalidation.

Uranium and Nuclear Sector. BUY / LONG. [SISTEM] URANIUM — Sweden 1.7 GW applications, Canada Bruce C 300 million dollar commitment, Natrium construction underway, NRC licensing acceleration all constitute independent structural nodes. URANIUM 6.19 percent above 30-day average. Data: Yahoo Finance UX=F. Invalidation condition: multiple major SMR project cancellations or NRC process reversal. Time horizon: LONG. [SISTEM] NUCLEAR_SMR — secondary with higher volatility, monitor. [SISTEM] NUCLEAR_UTIL — Duke Energy 97 percent capacity factor confirms existing fleet profitability.

Oil Sector. AVOID / PAS. [SISTEM] OIL — Price 8.11 percent below average but Rystad re-escalation scenario prices oil at 180 dollars conditionally. Insufficient visibility to hold either direction. Invalidation condition: full confirmed Hormuz closure triggers LONG; verified deal triggers SHORT entry. Time horizon: KISA reassessment ongoing.

Iron Sector. SELL / SHORT. [SISTEM] IRON — 8.45 percent structural gap, Hormuz-driven industrial input cost increase and China demand compression both active. Invalidation condition: China announces large-scale infrastructure stimulus or Hormuz reopens fully. Time horizon: MEDIUM.

Copper Sector. BUY / LONG. [SISTEM] COPPER — AI data center demand and war-driven supply constraint operating in the same direction, Bloomberg Copper Intelligence confirmation. 2.82 percent above average. Invalidation condition: material slowdown in US data center investment commitments. Time horizon: MEDIUM.

Crypto. UNDERWEIGHT. [SISTEM] BTC — Risk appetite barometer collapsed; 10.40 percent gap shows structural weakness. Liquidity exiting conventional instruments did not rotate into crypto. Invalidation condition: Risk-on recovery with BTC return to average. Time horizon: KISA avoid.

Currencies. [SISTEM] USDTRY — Near average, no clean entry. Turkish FM Fidan’s NATO summit diplomatic positioning is live; July Ankara summit outcomes may move USDTRY. AVOID, reassess post-summit. [SISTEM] USDJPY — 159.74, partial upside; if Fed rate hike scenario proceeds, yen remains under pressure. LONG USDJPY preference low, reverses on risk-off rotation.

Defense and Cybersecurity. [MANUEL] Cybersecurity ETF (e.g. CIBR or BUG) — Bloomberg flagged Palo Alto and CrowdStrike earnings as test for the 37 percent sector rally’s durability. Causal link: elevated warfare frequency structurally increases cyber attack cadence; IRGC maritime operations and Russia’s large-scale cyber campaigns are simultaneously active. Data: Yahoo Finance CIBR / BUG. Invalidation condition: Palo Alto or CrowdStrike miss in upcoming earnings. Time horizon: MEDIUM.

THESIS VALIDATION MATRIX

[Thesis Element] | [Confirms if] | [Invalidates if] | [Observable by]

US-Iran talks collapsed, war prolonged | Iran again suspended talks, IRGC attacks continued | Formal and permanent ceasefire agreement, Hormuz reopened | Bloomberg daily; Hellenic Shipping Hormuz transit reports

NATG structural long valid | NATG remains 6 percent or more above average | Hormuz transit normalized, Qatar LNG capacity returned | OilPrice.com, Hellenic Shipping weekly fleet report

Uranium and nuclear structural expansion continues | SMR project approvals accelerated, production costs fell | Multiple major projects cancelled or regulator delayed | Power Magazine Nuclear, World Nuclear News weekly

IRON short direction maintained | Industrial PMI China continued declining | China announced large-scale infrastructure stimulus | Bloomberg China data, Hellenic Dry Bulk report

BTC not confirming risk appetite | BTC remained below average, VIX calm | BTC rose 5 percent or more above average | Yahoo Finance BTC, VIX daily

RISK CALENDAR

July 2026 Ankara NATO Summit — Trump attendance confirmed by Turkish FM Fidan; new diplomatic dynamic on US-NATO-Iran axis, reassessment point for USDTRY and regional defense spending.

First week June 2026 — Rubio congressional testimony concludes; war powers resolution and 1.8 billion dollar fund vote establish US military commitment threshold in Iran.

First two weeks June 2026 — Palo Alto and CrowdStrike earnings; continuation or breakdown of the 37 percent cyber rally determined in this window.

End August 2026 — Rystad 180-dollar scenario threshold; if full Hormuz closure did not occur, this level is not reached, confirming medium-term oil short thesis.

Second half 2026 El Nino onset — Panama Canal committed to full capacity but NOAA El Nino watch is active; if restrictions emerge, reassess LNG_EQ and SHIPPING immediately.

Year-end 2026 — Australia wheat harvest 26 percent lower delivery period; reassess WHEAT entry point for food inflation positioning.

This writing represents my personal analysis and opinions only. It does not constitute investment advice. All investments and trading activities carry risk and are the sole responsibility of the reader.